-

- No Comments

- December 5, 2025

How much do you have to reinvest in 1031 exchange

1. Introduction

If you’re a real estate investor looking to maximize profits and defer taxes, you’ve likely heard of a 1031 exchange. But how exactly does it work, and more importantly, how much do you need to reinvest to fully defer capital gains taxes?

Understanding the reinvestment requirements isn’t just a technical detail it’s a make-or-break factor in preserving your wealth. Reinvest too little, and you could face unexpected taxes; reinvest smartly, and you keep more of your hard-earned money working for you.

In this blog, we’ll break down the rules you need to follow, walk through detailed calculations, and provide practical examples to ensure your 1031 exchange is executed correctly. By the end, you’ll have a clear roadmap for reinvesting your proceeds efficiently and confidently.

2. Understanding 1031 Exchanges

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, allows real estate investors to sell a property and reinvest the proceeds into another similar (“like-kind”) property without immediately paying capital gains taxes. Essentially, it’s a tax-deferral strategy designed to help investors grow wealth over time.

Here are the key terms you need to know:

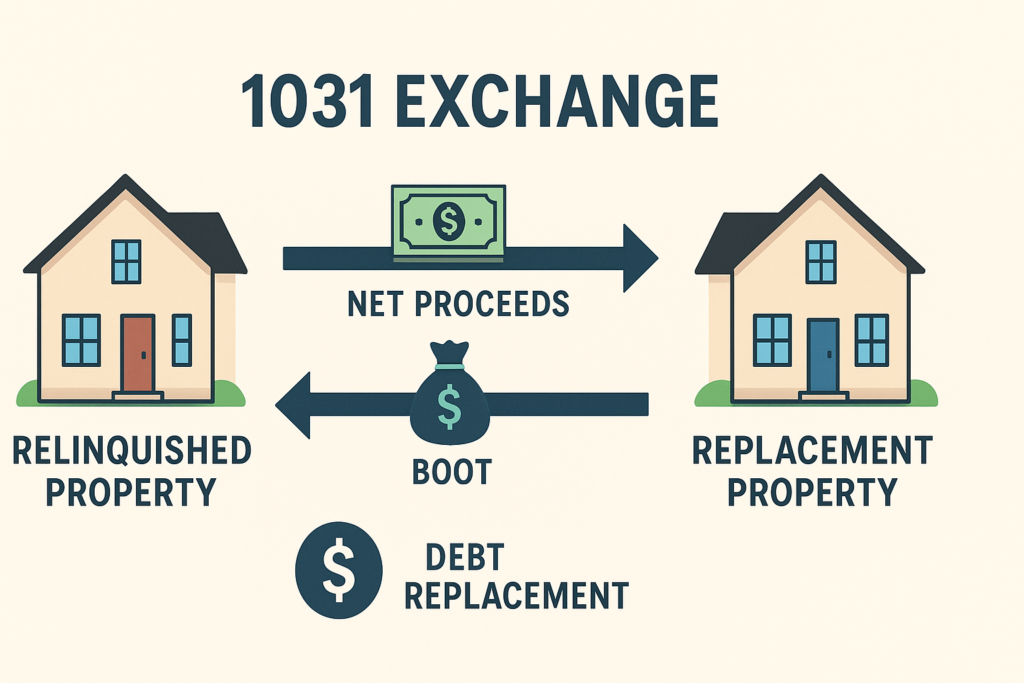

- Relinquished Property: The property you sell.

- Replacement Property: The new property you purchase with the proceeds.

- Net Proceeds: The money left after paying off debts and closing costs from the sale of your relinquished property.

- Boot: Any cash or non-like-kind property received during the exchange, which is taxable.

By properly following the reinvestment rules, a 1031 exchange lets investors defer taxes while moving equity into potentially higher-value properties. It’s a powerful tool—but only if you understand the mechanics and reinvest correctly.

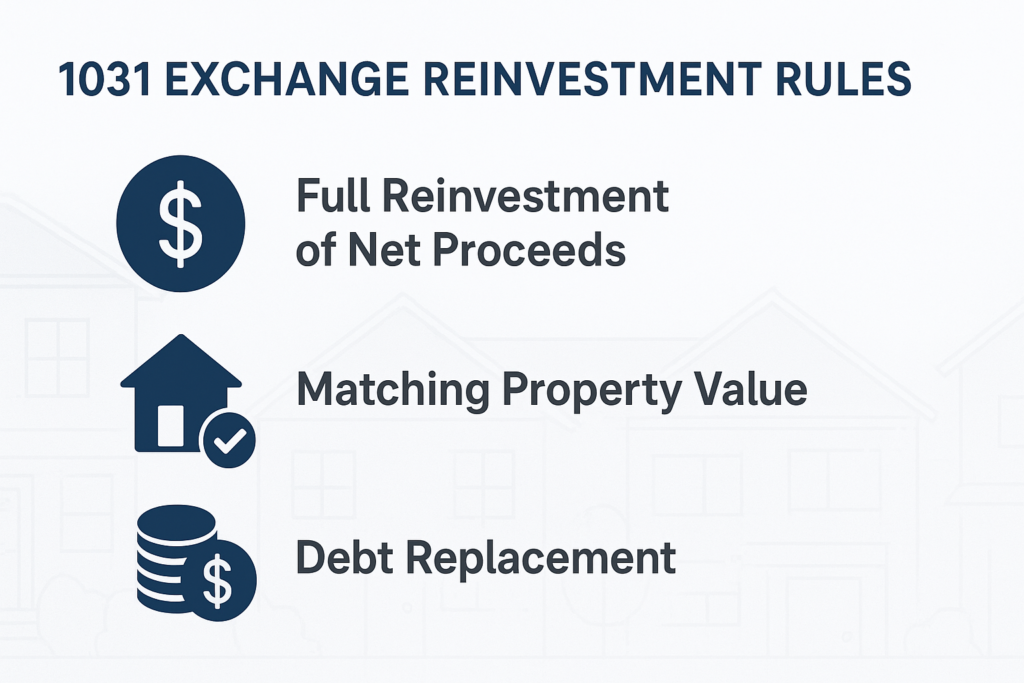

3. Key Reinvestment Rules

To fully defer capital gains taxes in a 1031 exchange, there are strict reinvestment rules that every investor must follow. Skipping any of these steps could trigger unwanted tax consequences. Let’s break them down.

3.1 Reinvest All Net Proceeds

The most critical rule of a 1031 exchange is this: you must reinvest 100% of the net proceeds from the sale of your relinquished property into one or more replacement properties. Net proceeds refer to the money left after paying off any existing mortgages and closing costs.

If you take any cash or receive property that isn’t “like-kind” (non-like-kind property), that portion is considered taxable boot. Simply put, taking even a small amount of cash out of the exchange could partially trigger capital gains taxes—defeating the purpose of the 1031 exchange.

3.2 Match or Exceed Sale Price

It’s not enough to just reinvest your net proceeds. The purchase price of the replacement property must meet or exceed the adjusted sale price of your relinquished property.

The adjusted sale price is calculated as the gross sale price minus selling expenses (like commissions, closing costs, and fees). For example, if you sold a property for $500,000 and paid $20,000 in closing costs, the adjusted sale price would be $480,000. Your replacement property must cost at least this amount to fully defer taxes.

Failing to meet or exceed this threshold can result in taxable boot, even if you reinvest all your net proceeds.

3.3 Match or Increase Debt Levels

1031 exchanges also require careful attention to mortgage or debt replacement. If your relinquished property had a mortgage, the debt on your replacement property must equal or exceed the debt that was paid off.

For instance, if you paid off a $100,000 mortgage on your sold property, the replacement property must carry at least $100,000 in debt. If the new property’s debt is lower, you’ll need to add cash to make up the difference. This ensures that the equity and debt balance is maintained, keeping your exchange fully tax-deferred.

Following these three rules—reinvest all net proceeds, match or exceed the sale price, and maintain or increase debt levels—is essential for a successful 1031 exchange. Even a small misstep can result in taxable boot and unexpected taxes.

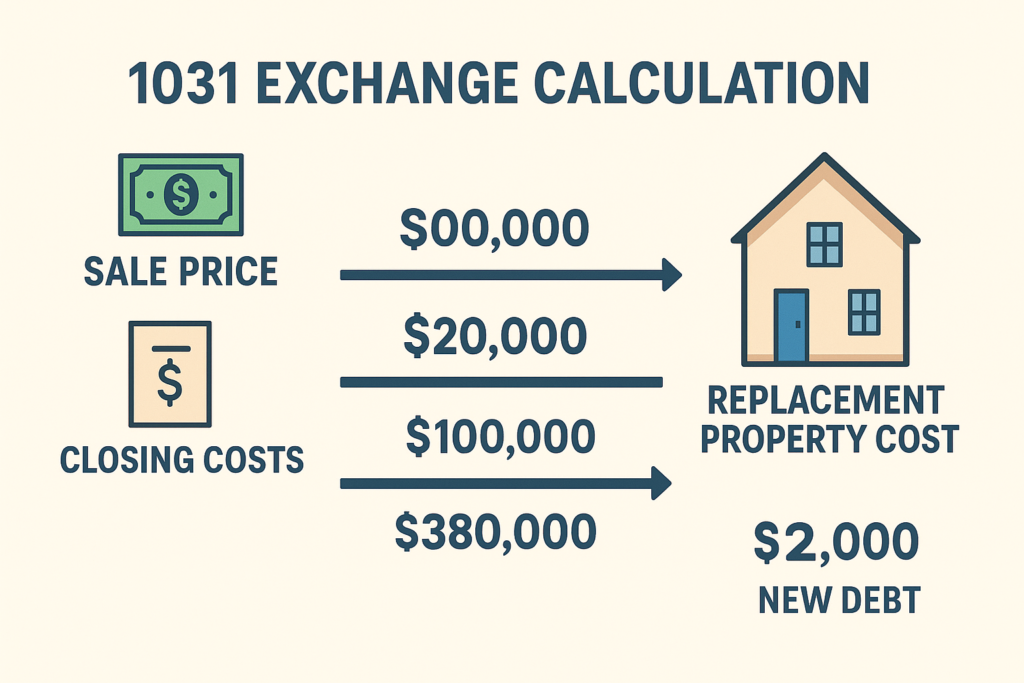

4. Example Calculation

Understanding the rules is one thing—but seeing them in action makes them crystal clear. Let’s walk through a practical scenario:

- Sale Price of Relinquished Property: $500,000

- Debt Paid Off: $100,000

- Closing Costs: $20,000

- Net Proceeds: $380,000

To fully defer capital gains taxes:

- Replacement Property Price: Must be at least $500,000 (match or exceed adjusted sale price).

- Reinvestment: All $380,000 of net proceeds must be reinvested.

- Debt Requirement: Must secure at least $100,000 in new debt (or add cash if the new property carries less debt).

Here’s a quick breakdown in table form for clarity:

| Item | Amount | Requirement / Notes |

| Sale Price | $500,000 | – |

| Closing Costs | $20,000 | Subtracted from sale price |

| Debt Paid Off | $100,000 | Must match or exceed in replacement property |

| Net Proceeds | $380,000 | Must reinvest 100% |

| Replacement Property | ≥ $500,000 | Adjusted sale price or more |

| New Debt | ≥ $100,000 | Or offset with cash |

Following this approach ensures the exchange is fully tax-deferred and avoids unintended taxable consequences.

5. Avoiding Taxable Boot

In 1031 exchanges, “boot” refers to any money or property received that is not like-kind. Boot is taxable and reduces the benefits of your exchange.

How boot can occur:

- Taking cash out of the exchange instead of reinvesting it.

- Purchasing a replacement property for less than the adjusted sale price.

- Failing to maintain or replace the debt on the relinquished property.

Tips to prevent boot:

- Reinvest all net proceeds into the replacement property.

- Match or exceed the adjusted sale price to avoid shortfalls.

- Maintain or exceed debt levels of the original property; add cash if necessary.

- Work with a qualified intermediary to ensure compliance.

- Keep detailed records of all transactions and calculations for IRS reporting.

By carefully following these steps, investors can fully defer capital gains taxes and avoid any unexpected taxable boot.

6. Role of a Qualified Intermediary

A qualified intermediary (QI) is an essential part of any 1031 exchange. They act as a neutral third party who handles the sale proceeds, ensuring that you never take possession of the funds, which is a strict IRS requirement. Without a QI, your exchange could be disqualified, and you could face immediate capital gains taxes.

How a QI ensures compliance:

- Receives and holds sale proceeds safely until you purchase your replacement property.

- Guides the reinvestment process, ensuring you follow the rules for net proceeds, property value, and debt replacement.

- Prepares proper documentation for IRS reporting, minimizing the risk of errors that could trigger taxable boot.

Tips for choosing a reliable intermediary:

- Confirm they are experienced with 1031 exchanges and licensed if required.

- Check references or reviews from other real estate investors.

- Ensure they provide clear guidance and transparent fees.

- Verify they maintain separate accounts for funds to avoid commingling.

- Look for a QI who is responsive and available throughout the exchange timeline.

A knowledgeable QI makes the difference between a smooth, fully tax-deferred exchange and costly mistakes.

7. Common Questions / FAQs

1. How much cash can I take out without triggering taxes?

Any cash taken out during the exchange is considered taxable boot, so ideally, you should reinvest all net proceeds to fully defer capital gains taxes.

2. What happens if I buy a replacement property for less than the sale price?

If the replacement property is less than the adjusted sale price, the shortfall is treated as taxable boot, and you may owe capital gains taxes on that amount.

3. How is debt replacement calculated?

The debt on the replacement property must equal or exceed the debt paid off on your relinquished property. If the new property carries less debt, you must add cash to make up the difference.

4. Can I do multiple replacement properties in one exchange?

Yes. You can acquire multiple replacement properties, but the combined purchase price must meet or exceed the adjusted sale price of the relinquished property, and debt/equity rules still apply.

5. Are there IRS forms I must file?

Yes. 1031 exchanges must be reported on IRS Form 8824 along with your annual tax return. Proper documentation ensures compliance and avoids penalties.

8. Related Topics / Further Reading

For more in-depth guidance and practical examples on 1031 exchanges, check out these trusted resources:

- How to calculate net sales proceeds for a 1031 exchange – Deferred.com – Step-by-step instructions for determining exactly what you need to reinvest.

- Reinvestment calculations and examples – Universal Pacific 1031 – Detailed numerical examples to help you understand reinvestment requirements.

- Debt replacement and mortgage boot rules – CR Capital 1031 – Learn how to handle mortgages and avoid taxable boot.

- IRS forms and reporting for 1031 exchanges – 1031.us – Official guidance on IRS reporting requirements, including Form 8824.

These resources provide both the technical details and practical examples to ensure your 1031 exchange stays fully compliant and tax-deferred.

9. Conclusion

Successfully completing a 1031 exchange hinges on three key principles:

- Full Reinvestment – Reinvest 100% of your net proceeds to defer capital gains taxes.

- Matching or Exceeding Property Value – Ensure the replacement property meets or surpasses the adjusted sale price of your relinquished property.

- Debt Replacement – Match or increase the debt carried on the original property, or add cash to cover any shortfall.

Careful planning and attention to these rules are essential. Even a small misstep can trigger taxable boot and reduce the benefits of your exchange.

To navigate these complexities confidently, it’s wise to consult a tax professional or work with a qualified intermediary. Their guidance ensures compliance, maximizes tax deferral, and keeps your real estate investments on track.

10. References

- Deferred.com: How Much to Reinvest – https://www.deferred.com/1031-exchange/how-much-to-reinvest/

- Universal Pacific 1031: Reinvestment Guide – https://www.up1031.com/reinvestment-guide/

- CR Capital 1031: Requirements – https://www.crcapital1031.com/1031-requirements/

- 1031.us: Rules – https://www.1031.us/rules/

- First Exchange: 1031 Rules – https://www.firstexchange.com/1031-rules/