-

- No Comments

- December 5, 2025

How much money do you need to never work again

1. Introduction

There’s a universal fantasy we all share at some point waking up one day, closing the laptop, silencing the notifications, and stepping into a life where work becomes optional. No deadlines. No meetings. Just freedom. But beneath the dream sits the one question everyone eventually asks: How much money do you actually need to never work again?

Here’s the truth: there’s no magic number. No universal “retire forever” jackpot. The real figure depends on just one thing your annual expenses. Not your income, not your age, not even your career. If you know what you spend each year, you can calculate the exact amount needed to fund your life indefinitely. And the math? Surprisingly simple.

2. The Core Formula: The 25x–30x Rule Explained

At the center of early retirement math is a principle called the 4% Safe Withdrawal Rule — the idea that if your money is invested in a balanced portfolio, you can sustainably withdraw 4% of your net worth every year, adjusted for inflation, without running out of money for 30+ years. It’s the backbone of the FIRE movement, financial independence planning, and every “never work again” calculator you’ll ever find.

And here’s where the shortcut comes in:

Your freedom number = your annual expenses × 25–30

Why 25 to 30?

Because if you withdraw 4% of your portfolio, you need about 25 times your yearly spending to safely sustain yourself. If you want a more conservative margin especially for early retirement or volatile markets multiply by 30 instead.

A few quick examples:

- Spend $40,000 per year? You’ll need roughly $1,000,000 to walk away.

- Spend $100,000 per year? Your target jumps to $2,500,000.

- Spend less? Your number drops dramatically.

- Spend more? Your freedom gets more expensive.

3. Step 1: Calculate Your True Annual Expenses

Before you can figure out how much money buys your freedom, you need to know one thing with absolute clarity: how much your life actually costs each year. Most people underestimate this sometimes by thousands because they track what’s obvious, not what’s real.

Start with the big, predictable categories:

- Housing: Rent or mortgage, utilities, maintenance, insurance.

- Food: Groceries, eating out, coffee runs that quietly add up.

- Transportation: Fuel, repairs, public transit, car payments.

- Healthcare: Insurance premiums, prescriptions, routine checkups.

- Lifestyle Costs: Subscriptions, clothes, travel, gifts, hobbies.

Once you’ve mapped your real annual spending, add a 20–50% safety buffer. Why? Because life is never as neat as spreadsheets. Medical surprises, emergency repairs, inflation spikes they all show up eventually. Planning for them upfront protects your long-term financial runway.

And don’t forget inflation. Even at a modest 3% yearly average, inflation compounds like interest just in the opposite direction. What costs $40,000 today could easily cost over $70,000 in 20 years. If your nest egg doesn’t account for this creeping pressure, you risk running short far earlier than expected.

Calculating your true annual expenses not your idealized version is the foundation of your “never work again” number. Get this part wrong, and every calculation that follows wobbles.

4. Step 2: Choose a Safe Withdrawal Rate (3% vs. 4%)

Once you understand your yearly expenses, the next decision is choosing a safe withdrawal rate the percentage of your investment portfolio you can pull out each year without depleting your wealth.

The classic benchmark is the 4% rule. It’s been battle-tested across decades of market data and assumes a well-diversified portfolio of stocks and bonds. Under normal conditions, withdrawing 4% annually allows your investments to grow enough to outpace inflation and sustain your lifestyle for 30 years or more.

But here’s where things get nuanced.

Many early retirees especially those planning for 40 to 60 years of retirement choose a 3% withdrawal rate instead. It’s more conservative, but it dramatically reduces the risk of running out of money, particularly during long market downturns. The trade-off? You need a larger nest egg.

Going above 4% might feel tempting (“Why not just take 5%?”), but the danger is real:

- You increase your exposure to sequence of returns risk — the threat of early market losses derailing your entire plan.

- You put your portfolio under heavier strain in years where markets underperform.

- Your cushion for inflation and emergencies shrinks dramatically.

Choosing between 3% and 4% is ultimately a question of risk tolerance, retirement age, and lifestyle stability. The safer the withdrawal rate, the pricier the freedom but also the more secure.

5. Step 3: Understand Your Investment Strategy

Your “never work again” number doesn’t live in a savings account it lives in an investment strategy designed to grow, protect, and sustain your wealth for decades.The way you invest directly shapes how long your money lasts and how confidently you can rely on it.

Index Funds (7–8% average returns):

These are the backbone of most financial independence portfolios. Low fees, broad diversification, and long-term reliability make index funds a powerhouse for compounding growth. Over decades, they typically outperform most actively managed funds, which is exactly what you want when your money needs to last forever.

Bonds (around 3% returns):

Bonds don’t deliver thrilling returns, but they offer something arguably more valuable: stability. When markets dip, bonds help soften the blow, giving your portfolio a smoother ride. For retirees, this stability reduces the risk of withdrawing during downturns a critical safeguard for long-term sustainability.

Real Estate (passive income potential):

Rental properties can serve as an additional income stream that reduces pressure on your portfolio. Whether it’s long-term rentals, short-term Airbnb-style units, or even REITs, real estate introduces cash flow that helps offset inflation and unpredictable market cycles.

Regardless of your mix, the golden rule stands:

Protect your principal.

The moment you start dipping into the core of your nest egg not just the returns you shorten the lifespan of your financial freedom. A strategic, diversified investment plan is what keeps the engine running, year after year.

6. How Age and Lifespan Change the Number

Your retirement age dramatically shifts how much money you need to walk away from work forever. The earlier you retire, the longer your money must last and the larger your freedom number becomes.

Retiring at 35:

You could easily need 50+ years of financial support. That’s half a century of market cycles, inflation, healthcare changes, and unexpected life events. For that reason, early retirees often lean toward the conservative end of the spectrum using a 3% withdrawal rate and a 30x–33x multiplier. Even a frugal lifestyle could still require $1.25 million or more.

Retiring at 60:

Now your portfolio only needs to support you for 20–30 years. On top of that, you can factor in potential income sources like Social Security, pensions, or part-time work. This naturally lowers the pressure on your investments, making a 4% withdrawal rate more realistic. For many, even $500,000–$1 million may be enough, depending on lifestyle.

The key concept here:

The longer your retirement, the more conservative you must be.

Your age determines your time horizon. Your time horizon determines your risk.

And your risk determines your final “never work again” number.

7. Sample “Never Work Again” Targets (Table Section)

Below is a simple snapshot of how annual spending translates into your freedom number under both the 4% and 3% withdrawal rules. This table anchors the concept in real numbers so you can easily see where you fall.

| Annual Expenses | 4% Rule (25x) | 3% Rule (33x) | Notes |

| $40,000 | $1,000,000 | $1,330,000 | Frugal single person |

| $60,000 | $1,500,000 | $2,000,000 | Comfortable family |

| $100,000 | $2,500,000 | $3,330,000 | Urban professional |

These numbers are starting points your real target depends on dozens of personal variables, which brings us to the next section.

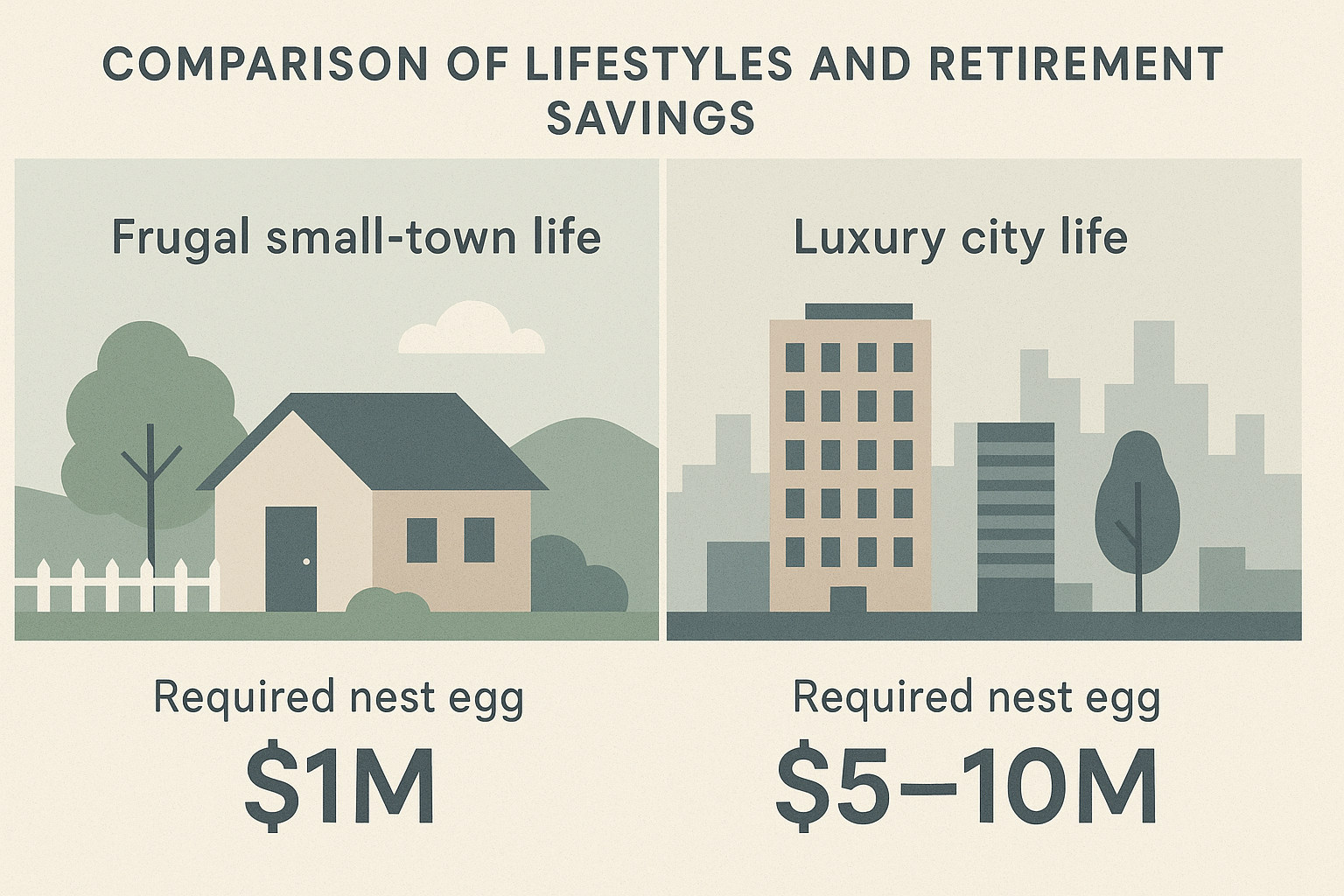

8. Lifestyle, Location & Health: Hidden Variables That Change Everything

Your annual expenses aren’t the whole story. Where you live, how you live, and your long-term health can dramatically inflate or shrink your “never work again” number.

Low-cost or frugal living:

If you’re in a modest U.S. town, live simply, and avoid big-ticket luxuries, $1–2 million could realistically sustain you for life especially with a 3–4% withdrawal strategy.

High-cost cities or luxury lifestyles:

If you’re in places like New York, San Francisco, London, or Dubai, or if you enjoy frequent travel, designer shopping, premium dining, or private schooling, your target jumps fast. For some, the freedom number realistically lands between $5–10+ million.

Healthcare:

This is the biggest wildcard. Chronic conditions, rising insurance premiums, long-term care, or specialist treatments can add tens of thousands to your yearly costs — especially before Medicare or government support kicks in. Early retirees must plan for this explicitly.

Family size & responsibilities:

Kids, aging parents, and multigenerational obligations can increase your annual expenses dramatically. A single 25-year-old nomad might need one number; a family of five in a metro area needs something entirely different.

Lifestyle isn’t just a detail — it’s the weight that tilts the entire equation. You can control your expenses, but you must be honest about your reality.

9. Common Mistakes People Make When Calculating Their Number

Most people don’t get their “never work again” number wrong because of math — they get it wrong because of assumptions. Here are the biggest pitfalls that quietly inflate risk and shrink your financial runway:

Underestimating expenses:

People often calculate based on their current lifestyle instead of the lifestyle they’ll actually want later. Travel, kids, hobbies, medical care, home repairs — these add up fast.

Forgetting long-term inflation:

A 3% annual inflation rate may look harmless, but over 20–30 years, it compounds aggressively. What costs $40,000 today could cost $65,000 or more in a few decades. Many people ignore this entirely.

Assuming unrealistic investment returns:

Planning for consistent 10–12% returns is fantasy land. Markets fluctuate, crashes happen, and sustainable planning usually assumes 7–8% for stocks and far lower for bonds.

Ignoring big surprise costs:

Healthcare emergencies, dental surgeries, family responsibilities, relocations, and home maintenance can demolish a withdrawal plan if not included in your buffer. This is why a 20–50% safety margin is essential.

Avoid these mistakes, and your number becomes far more accurate — and far more reliable.

10. Build Your “Never Work Again” Plan: A Mini Roadmap

Here’s a tight, actionable roadmap you can follow to calculate (and work toward) your freedom number:

1. Determine your annual spending.

Track every category — housing, food, transportation, insurance, travel, healthcare, fun money. Then add a 20–50% buffer for inflation and surprises.

2. Pick a withdrawal rate.

Use 4% for standard retirement or 3% if you want a safer, early-retirement-friendly option.

3. Calculate your total nest egg.

Multiply your annual expenses by 25x (for 4%) or 33x (for 3%).

This gives you the exact amount needed to stop working forever.

4. Align your investments for sustainable long-term income.

Build a diversified strategy using index funds for growth, bonds for stability, and real estate for passive income. Most importantly: protect the principal and manage risk.

With these four steps, the abstract dream of “never working again” becomes a concrete, calculable plan — something you can build toward with confidence and clarity.

11. Simple Calculator Template (Embed Section)

Use this simple formula-based calculator (placeholder for embedding):

- Step 1: Enter your monthly expenses.

- Step 2: Calculator multiplies by 12 → gives annual spending.

- Step 3: Choose your preferred factor: 25× (standard) or 30× (more conservative).

- Step 4: Your Financial Freedom Number updates instantly based on:

Freedom Number = Annual Spending × 25 or 30

Embed note: “Enter expenses → number auto-updates.”

12. Additional Resources / Recommended Reading

Here are solid sources that help you go deeper:

- Reddit Discussions: Community insights on FIRE, real-life case studies, and spending strategies.

- 4% Rule Guides: Forbes articles and YouTube explainers that break down sustainable withdrawal math.

- Expert Analyses:

- DebtFreeDr

- Bankrate

- CreditNinja

All provide clear breakdowns on long-term planning, investing, and retirement safety margins.

- DebtFreeDr

13. Conclusion

Your financial freedom number is not random it’s built on your expenses, your risk tolerance, and your lifestyle goals.

At the end of the day, financial independence is a mix of simple math + intentional living. Know your number, plan for it, and let your strategy guide your future freedom.

Frequently Asked Questions (FAQ)

1. How do I know if I’m tracking my expenses accurately?

Track all categories — housing, food, travel, healthcare, subscriptions, and fun money. Add a 20–50% buffer for surprises and inflation to capture your true annual spending.

2. What’s the difference between the 3% and 4% withdrawal rules?

4% is standard for most retirees, allowing your portfolio to last ~30 years. 3% is safer, especially for early retirees or longer horizons, but it requires a larger nest egg.

3. Can I retire early with less than $1 million?

It depends on your lifestyle, location, and risk tolerance. Frugal living in low-cost areas may allow early retirement with lower savings, but higher-cost lifestyles need millions.

4. How do inflation and healthcare costs affect my number?

Inflation compounds yearly, and healthcare expenses can spike unexpectedly. Both factors increase the nest egg you need to maintain financial freedom safely.

5. Do I need to invest in stocks, bonds, and real estate to never work again?

A diversified investment strategy is crucial. Index funds provide growth, bonds add stability, and real estate can supply passive income — all while protecting your principal.